Gas production from small onshore and offshore gas fields in the Netherlands threatens to collapse completely in the coming decade, mainly as a result of a deteriorating investment climate. This will lead to higher imports of LNG and Russian gas than currently foreseen, which will have a strongly negative effect on greenhouse gas emissions. Those are the major conclusions of a new report from independent researchers Jilles van den Beukel and Lucia van Geuns published by The Hague Centre for Strategic Studies (HCSS), writes Natural Gas World magazine.

Dutch gas policy has received a lot of publicity in recent years. The Dutch government decided in 2018 to phase out production from the giant Groningen field, which is now expected to be closed down in 2022. Nevertheless, production from small fields (i.e. all fields except “Groningen”) is continuing in the Netherlands. Although production from these fields has been declining since the turn of the century, mainly for geological reasons, they are still expected to deliver some 10 to 12 bn cm by 2030, according to official estimates.

These estimates, however, are called into question by Van den Beukel and Van Geuns, two well-known Dutch energy analysts, both with a geological background. In their paper, “The deteriorating outlook for Dutch small natural gas fields”, published by HCSS, an independent geopolitical think tank, the researchers argue that small fields production is more likely to be 5 bn cm by the end of the decade, and may very well collapse altogether.

Virtual standstill

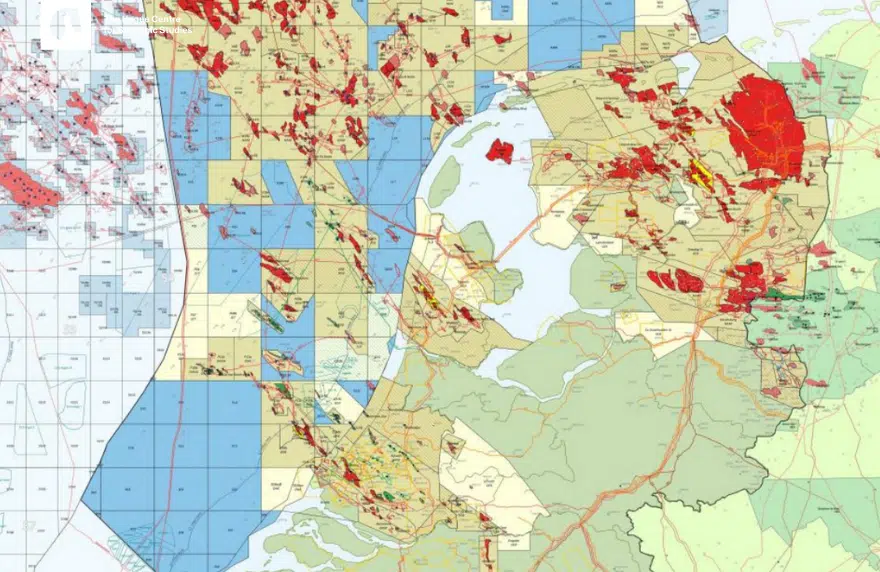

The researchers note that exploration activity to find new offshore fields has dwindled to 20% of what it was in 2012. Exploration activity onshore has come to a virtual standstill, even though “there is no geological reason” for this “dramatic decrease”. They observe that the “exploration potential has stayed at a relatively constant level” and there is still “about 200-300 bn cm of (risked) exploration potential from the Dutch offshore.”

The two researchers ascribe this decline in exploration activity to a series of adverse policies from the Dutch government which have shaken the confidence of operators in Dutch gas prospects. These include negative tax measures (a “significantly worse tax regime than in the UK”), regulatory obstacles and delays (they cite the example of a discovery made offshore in 2017 which is expected to see first production in 2023 at the earliest), new very strict environmental legislation banning nitrogen oxide emissions, and strong resistance from local authorities to new onshore exploration and production activities.

These anti-gas measures must be seen in the context of “a (negative) change in the public image of natural gas in the Netherlands”, note the authors. In an earlier paper for HCSS, published in February 2019, Van den Beukel and Van Geuns had observed that the gas industry in the Netherlands has lost its “social license to operate” as a result of public concerns over induced earthquakes and climate change. The authors see no reason to expect any improvement in the investment climate. “If anything,” they write, “things are more likely to get worse rather than better.”

Negative spiral

The negative political and public sentiments towards natural gas production in the Netherlands threaten to set in motion a negative spiral, the authors warn, as operators become increasingly hesitant to invest in the Dutch gas sector. “It is becoming more difficult for Dutch subsidiaries to obtain funding from international head offices,” write Van den Beukel and Van Geuns. Making matters worse is that gas prices are expected to stay low in the medium term and production costs are likely to go up as “decreasing production results in higher unit operating costs”.

Van den Beukel and Van Geuns further note that a recent “lookback” study from EBN, the state entity that is a non-operating partner in all Dutch gas fields, shows that over the last decades official predictions of future production from the small fields have consistently overestimated real production.

For these reasons, the two researchers believe that the current official outlook of 10-12 bn cm of small fields production by 2030 is likely to be far too high. They believe 5 bn cm is more likely and do not rule out that “Dutch gas production in 2030 is about to cease completely”. They add that “this scenario becomes more likely if natural gas prices stay at the current low levels for an extensive period of time.”

Higher imports

According to the authors, a collapse of Dutch gas production would have adverse economic and environmental effects. They observe that gas consumption in the Netherlands as well as in the neighbouring countries is relatively stable and likely to remain so, as gas loses market share to renewables, but gains market share from the planned phaseout of coal power plants (both in the Netherlands and Germany) and nuclear power (in Germany). This implies that lower production in the Netherlands will necessarily lead to higher imports of LNG and Russian gas.

This is already happening, Van den Beukel and Van Geuns note. From 2014 to 2018 annual Gazprom pipeline exports to Europe increased from less than 150 bn cm to over 200 bn cm. In 2018 and 2019, the import of LNG into Europe started to rise significantly. European imports of LNG are now expected to be around 100 bcm for the 2020-2025 period, double the level of 2010-2017.

Higher imports of LNG and Russian gas not only cost money, they also have a negative effect on greenhouse gas emissions, the authors observe. While lower gas production in the Netherlands leads to lower national greenhouse gas emissions, the effect on total greenhouse gas emissions is the opposite. “Replacing Dutch gas by important gas results in significantly higher upstream emissions”, the authors note, as Russian gas and shale gas have much higher methane leakage.

In their paper, Van den Beukel calculate that “the replacement in the EU of Dutch gas by Russian gas and LNG negates all progress that has been made by increasing the share of solar and wind in the Dutch power mix.” The authors argue – in a separate opinion piece – that for this reason alone the government should take action to “save Dutch gas production.”

This article by Karel Beckman was originally published in Natural Gas World magazine, Vol.5, issue 3.

Related Content