The much anticipated “Draghi-report” published earlier this month has by now made its way into most parliaments, cabinet offices and boardrooms. The almost 400 pages of analysis and recommendations provide a stark warning for the EU to clean up its economic and industrial act.

The conclusions from the main report (section A) have already been covered in op-eds, policy briefs and essays, but section B of the report, which contains sector-specific in-depth analyses, still contains valuable nuggets of information.

Many of the sectors mentioned in the report are direct research areas of The Hague Centre for Strategic Studies. In this Draghi Report Series, we decided to ask our experts for their views on specific sections of this high-profile report.

For the sixth installment of our Draghi Report Series, we asked strategic advisors Lucia van Geuns and Jilles van den Beukel for their take on the report’s section on Energy.

– Which policy recommendations do you think are the strongest, and why?

We fully support the need to streamline licensing procedures for the new energy system. This is essential to accelerate the energy transition, which we must pursue both to combat climate change and to strengthen EU’s independence in relation to the US and China. Europe is currently facing strategic energy dependencies and excessive regulation, which pose significant barriers to its competitiveness.

Lucia van Geuns: “This is a no-nonsense report that confronts the tough decisions that need to be made. It advocates for a more integrated and efficient European energy market. Draghi’s suggestion that the EU may have to relinquish the solar panel industry is perhaps difficult to accept, but there is merit to it: the gap with China is insurmountable here. The EU should commit to supporting the European automotive industry (too big to fail), battery manufacturing (given the importance for EVs), and wind turbines (better EU position than solar).”

Jilles van den Beukel: “In contrast to collective procurement (discussed below), I have more positive expectations from Draghi’s measures to prevent net congestion and putting into place ‘power purchase agreements’ (PPA’s) and ‘contracts for difference’ (CFD’s), for example. In the gas market, the basic problem of the EU, its high dependency on imported fossil fuels, is there to stay. The painful consequences of this dependency will not be solved by collective procurement of gas. Additionally, reducing energy taxes is urgently needed.”

– Is there anything missing in the policy recommendations? What would you add?

Jilles van den Beukel: When it comes to gas, it’s important to remember that the largest profits in recent years have been made in Qatar. Draghi highlights the increased profits of trading houses, but this isn’t surprising given their significantly higher total turnover. If these trading houses were smart, they likely secured long-term contracts at lower prices – and you can’t blame them for that. Draghi also suggests that collective procurement could have been a solution or made a difference during the energy crisis. However, high prices actually led to reduced demand and increased LNG imports to Europe, replacing Russian gas. In this case, collective procurement wouldn’t have had much impact.

Lucia van Geuns: On oil, production cuts from the OPEC-countries do matter for the EU, due to its import dependence. In general, it is advisable to fight fossil fuels mainly on the demand side. CO2 pricing and reducing emission rights work better than imposing restrictions on the oil and gas industry, which shifts pricing power back to OPEC (oil) or Qatar and Russia (gas).

– Which figure or data point in the report did you find most insightful, and why?

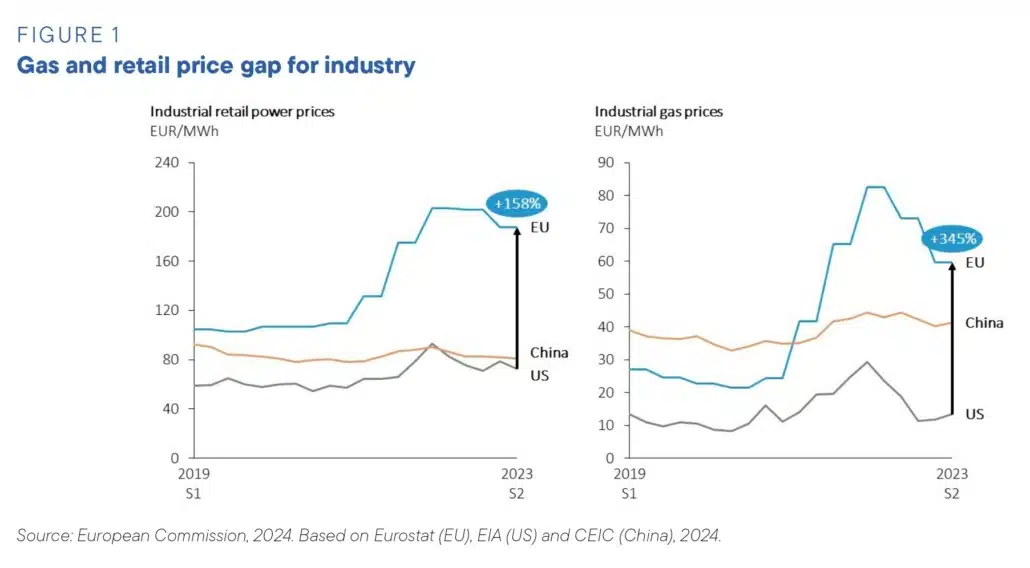

Figure 1 of the report clearly outlines EU’s price gap between China and the US for gas and electricity. This has created a significant competitive disadvantage for European companies compared to, especially, the US.

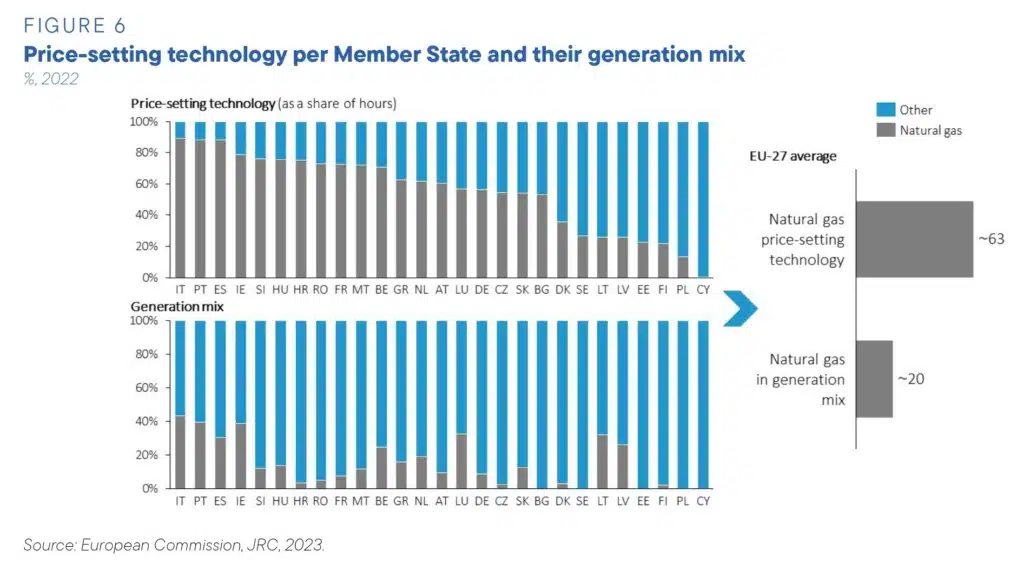

Also, Figure 6 is important as it shows the dominant influence of natural gas on electricity prices in the EU. Gas makes up around 20% of the energy mix, yet in 63% of the cases, electricity prices are being determined by gas prices (merit order). Not everybody is aware of this!

– How do you view the feasibility of these plans in a European context?

Lucia van Geuns: The report stresses the need for the EU to accelerate the transition to renewable energy sources and improve energy efficiency across all sectors in order to reduce its energy dependance. At the same time, the Draghi report emphasizes the negative impact of, among others, high prices on the competitiveness of the EU industry, and advocates an assertive industrial policy based on strategic importance.

Jilles van den Beukel: Realising these plans and achieving the goals is going to be quite a challenge. Decarbonisation, ensuring security of supply and affordability of energy can go hand in hand. We endorse the pragmatism of Draghi’s insights and solutions of the electricity markets more than those on the gas market – collective procurement is not going to work in the EU. With the LNG market expected to expand in the coming years, a new crisis is more likely to be seen in the field of electricity (severe grid congestion) than in the field of gas.

Stay tuned for the next issue of the Draghi Report Series by HCSS, where we invite experts to discuss other sectorial policies in Mario Draghi’s report “The future of European competitiveness”.

Read the previous installments here:

- Draghi Report Series | Patrick Bolder on Space

- Draghi Report Series | Benedetta Girardi on Semiconductors

- Draghi Report Series | Han ten Broeke and Ron Stoop on Automotive

- Draghi Report Series | Irina Patrahau and Michel Rademaker on Critical Raw Materials

- Draghi Report Series | Tim Sweijs and Frank Bekkers on Defence

Related Content