The US has made reviving its own manufacturing industry a core ambition. In Trump’s second term, tariffs play a central role in attracting investment, production, and employment to the US. One year later, have these tariffs strengthened domestic manufacturing?

By Geoffroy Feij, Policy Advisor International Business at FME & Ron Stoop, Strategic Analyst at The Hague Centre for Strategic Studies (HCSS).

In brief:

- It has been one year since Trump announced increased tariffs for all trading partners on ‘Liberation Day.’

- Since then, investment, construction spending, and employment have all trended downward.

- Production growth remains marginal, and procurement surveys point to sustained industrial weakness.

Introduction

The COVID-19 crisis, the growing weaponisation of trade, and rising geopolitical tensions have led countries to increasingly prioritise strengthening their own manufacturing industries. The aim is to reduce vulnerability to economic coercion or sudden supply disruptions of critical goods, such as semiconductors, critical raw materials, or green technologies.

Countries have a broad range of policy instruments at their disposal to support manufacturing. Among these, tariffs are gaining prominence. Between 2024 and 2025, the global number of tariffs with at least partial focus on manufacturing rose from 135 to 289.[1] This growth is largely attributable to the US. President Trump’s trade policy translated into a sixfold increase in the average American tariff by late December 2025 compared to the beginning of that year.[2]

The EU also appears increasingly comfortable with higher tariffs. EU Trade Commissioner Šefčovič recently argued for making it easier within the World Trade Organization (WTO) to raise tariffs.[3] A senior French government official also floated the idea of a general European tariff of 30 percent on all Chinese products.[4] This trend is particularly relevant for the Netherlands, which has an open, trade-oriented economy and is home to the sixth largest manufacturing industry in the EU.[5]

Economists have previously argued that tariffs are a blunt instrument for strengthening the American economy. Sommer and Meijerink concluded on the basis of economic theory that tariffs are not the answer to reinvigorating the American economy: technological change explains manufacturing job losses more convincingly than trade deficits, which means tariffs are not the right response.[6] This article builds on that argument by taking not theory but early data as the benchmark.

Given that the European debate on tariffs is evolving rapidly, it is useful to examine the initial effects of American tariffs since ‘Liberation Day’ (2 April 2025) on US manufacturing. Although the observation period is relatively short and the full impact has not yet materialised, Europe can draw lessons from the American policy approach and assess how effective tariffs have been in achieving their stated objectives.

The US manufacturing push

Strengthening the manufacturing sector serves not only as an economic policy goal but also as a core component of national security policy. Trump’s ambition to reinvigorate American manufacturing did not emerge in a vacuum — it builds on a broader policy direction in which his predecessor Biden had already made re-industrialisation a central priority. The US has seen a substantial share of its industrial production capacity disappear over recent decades. Since 1980, nearly 8 million manufacturing jobs have been lost.[7] Today, only 12.6 million people work in manufacturing, representing 7.7 percent of the American workforce.[8] While the US accounted for 25 percent of global manufacturing output in 2000, this share is projected to fall to 11 percent by 2030.[9] This job loss is part of a broader global trend in which technological progress and higher productivity reduce direct employment, though competitors such as the EU and China employ far more manufacturing workers, at 30 million and 120 million respectively.[10]

As a result, the US is increasingly dependent on foreign supply chains for strategic goods. Today, the US accounts for just 0.2 percent of global commercial shipbuilding, produces 10 percent of the world’s semiconductors, and is entirely dependent on foreign sources for twelve critical raw materials.[11] This creates risks for military readiness.

Liberation Day

“April 2nd, 2025, will forever be remembered as the day American industry was reborn,” declared President Trump upon announcing a minimum tariff of 10 percent for all trading partners, plus additional ‘reciprocal tariffs’ of 11 to 50 percent on 57 specific partners.[12] According to President Trump, these tariffs were intended to give domestic industry a powerful boost.

To further protect manufacturing, Trump also made extensive use of Section 232 of the Trade Expansion Act of 1962. This provision grants the US president the authority to impose tariffs and other trade measures, following an investigation, when certain imported goods pose a threat to national security. Of the fourteen Section 232 investigations launched to date, thirteen focus on manufactured products, including medical devices, wind turbines, and robotics.[13] This led to tariffs in 2025 on steel and aluminum (25 percent from 4 March, rising to 50 percent from 4 June), cars and auto parts (both 25 percent, from 3 April and 3 May respectively), copper (50 percent from 1 August), and trucks (25 percent from 1 November). On 15 January 2026, the US additionally imposed tariffs of 25 percent on specific semiconductors.

Since Liberation Day, the US has granted partial exemptions to a significant number of trading partners, both under the reciprocal tariff framework and under measures arising from Section 232 investigations. These exemptions largely resulted from trade deals the US concluded with 19 trading partners.[14] By December 2025, partial exemptions applied to $1,700 billion worth of imports, while $1,600 billion in imports remained subject to the originally announced tariff rates.[15] Nonetheless, the average US tariff in December 2025 remained historically elevated at 13 percent.[16] Even after the US Supreme Court ruling on the unlawfulness of the reciprocal tariffs and the introduction of a new 10 percent tariff, the average remained at 11.6 percent.[17]

No revival of American manufacturing

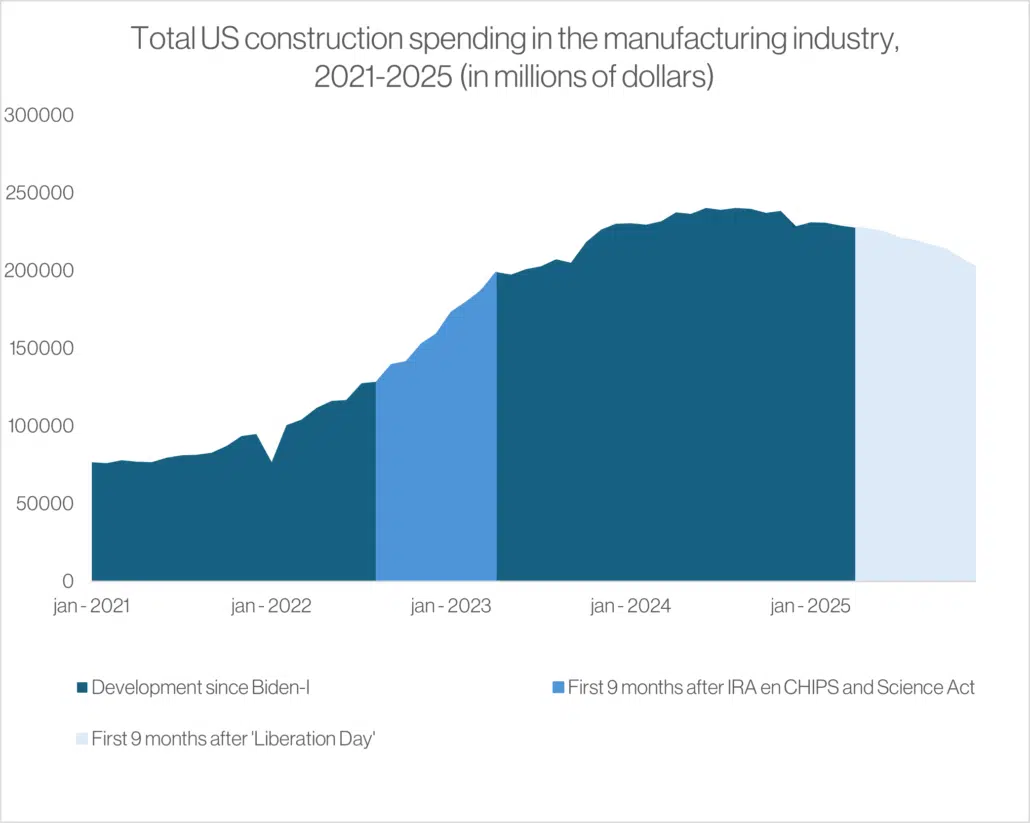

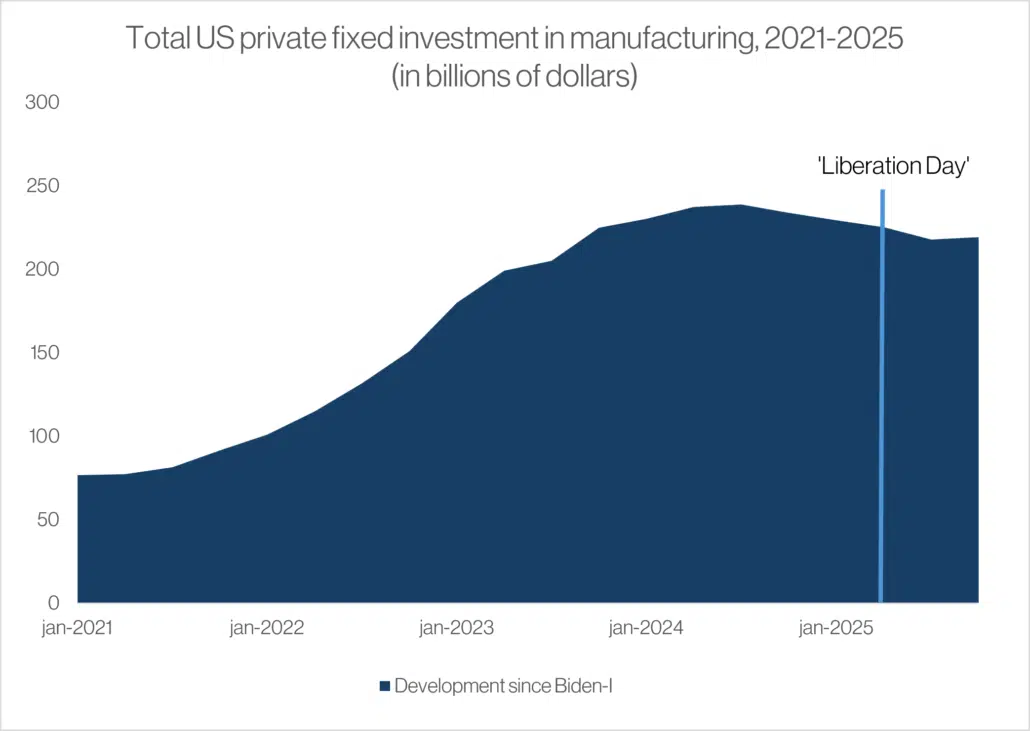

Despite the higher tariffs, multiple indicators show that a genuine manufacturing revival has not materialised. Two important indicators are construction spending on new industrial projects and the level of private fixed investment.[18] Between April and December 2025, both showed a downward trend (Figure 1 and Figure 2). Construction spending and private fixed investment fell by 11.1 and 4.6 percent respectively over this period.

Figure 1: US Construction spending between 2021 and 2025

Figure 2: US private fixed investment in manufacturing 2021 and 2025

Although lagging investment might seem understandable, since investment announcements take time to translate into actual spending, government interventions can generate rapid effects: Figure 1 shows that nine months after the Inflation Reduction Act and the CHIPS and Science Act entered into force, construction spending and private fixed investment were 55 and 30 percent higher respectively.

Employment and production volume data tell the same story of an absent renaissance. Between April and December 2025, manufacturing employment fell every single month, resulting in a net loss of 77,000 jobs: a decline of 0.6 percent.[19] Over the same period, production volume increased, but only marginally: by 0.8 percent.[20]

Finally, business cycle indicators show no signs of an upswing either. A monthly purchasing manager survey index recorded uninterrupted contraction between April and December 2025, with December 2025 reaching its lowest level since October 2024.[21]

Trump’s approach appears to be failing

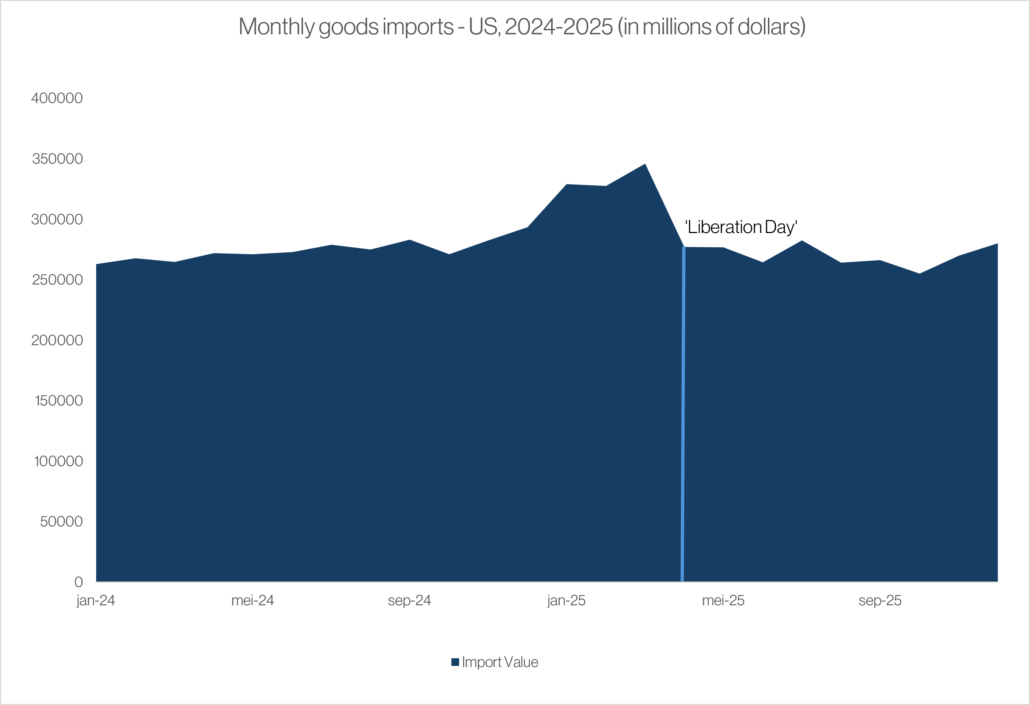

One explanation for the absent manufacturing revival lies in the broad scope of the tariffs combined with the structure of American imports. Roughly 50 percent of US imports consist of intermediate goods: inputs that companies need to produce finished products.[22] In other industrial countries such as Germany, China, and Japan, this share is between 15 and 20 percent.[23] Imports of these intermediate goods do not displace American manufacturing—they enable it. Despite all the tariffs, US goods imports in the final quarter of 2025 fell by only 3.5 percent compared to the last quarter of 2024 (Figure 3). Because the tariffs are broadly designed and therefore apply substantially to essential intermediate goods imports as well, it appears that American businesses themselves are primarily bearing the higher costs.

Figure 3: Monthly Goods imports – US

In addition, tariffs stimulate demand for American goods, but supply cannot easily keep pace given the labour shortages the US is facing. In December 2025, there were 433,000 manufacturing job vacancies, amounting to 3.4 percent of all workers in the sector.[24] This is against a backdrop in which the sector is estimated to need 3.8 million additional workers between 2024 and 2033, with the risk that roughly half of this demand will go unmet.[25] These shortages also clash with Trump’s strict immigration policy. 3.1 million US manufacturing workers were born abroad.[26] The semiconductor industry in particular, a rapidly growing strategic sector, is heavily dependent on foreign-born skilled workers.[27] A group of American national security experts sounded the alarm as early as 2022: “America’s efforts to onshore critical supply chains will not succeed unless it also onshores the talent necessary to compete.”[28]

Finally, the unpredictability of American trade policy undermines investment confidence. Uncertainty around trade policy is particularly effective at suppressing investment.[29] Since Liberation Day, this uncertainty has intensified sharply: between April and December 2025, the US Monthly Economic Policy Uncertainty Index averaged 264 percent higher than during the same period in 2024.[30] Trump changed tariff levels at a rapid pace, repeatedly threatened further increases, and introduced partial exemptions with minimal lead time. The interval between announcement and implementation was frequently very short. In one instance, just a single working day separated Trump’s announcement adding over 400 additional products, collectively accounting for $210 billion in import value in 2024, to the 50 percent steel and aluminum tariffs.[31]

Conclusion

One year after Liberation Day, investment, construction, business cycle, and labour market indicators give no sign of a revival in American manufacturing. Given the structure of US imports, labour market tightness, and the volatility of trade policy, it is far from certain that continuing the current approach will achieve the intended re-industrialisation.

The absent revival of American manufacturing illustrates the limitations of broad-based tariffs. They also heighten diplomatic tensions and tend to produce economically unpredictable outcomes. For Europe, generalised tariffs are therefore a blunt and unreliable instrument for strengthening competitiveness and export performance.

About the authors

- Geoffroy Feij works as a policy advisor for FME, the Dutch employers’ organization for the technology industry, representing over 2,100 members. His work focuses on policy advocacy in areas related to trade policy, export promotion, economic security, and corporate responsibility. He has an academic background in global political economy.

- Ron Stoop is a Strategic Analyst at HCSS, specialising in geo-economics. His work focuses on industrial policy, clean technologies for the energy transition and the defence industry. His areas of expertise include clean technologies, industrial policy, raw materials, trade policy and macro-economics.

[1] Global Trade Alert, ‘Global Trade Alert – Monitoring Policy Changes That Affect Global Trade’, accessed 29 March 2026, https://globaltradealert.org/.

[2] Mary Amiti et al., ‘Who Is Paying for the 2025 U.S. Tariffs?’, Liberty Street Economics, ahead of print, 12 February 2026, https://doi.org/10.59576/lse.20260212.

[3] Peter Foster and Andy Bounds, ‘EU Seeks to Reform WTO “Most Favoured Nation” Trade Rules’, Financial Times, 21 January 2026.

[4] Haut-commissariat à la stratégie et au plan, ‘L’industrie Européenne Face Au Rouleau Compresseur Chinois’, 9 February 2026, https://www.strategie-plan.gouv.fr/publications/lindustrie-europeenne-face-au-rouleau-compresseur-chinois.

[5] Eurostat, ‘Sold Production, Exports and Imports’, accessed 29 March 2026, https://ec.europa.eu/eurostat/databrowser/product/view/ds-059358?category=prom.

[6] Konstantin Sommer and Gerdien Meijerink, De (on)mogelijke redenering achter Trumps handelsbeleid, 11 December 2025, https://esb.nu/de-onmogelijke-redenering-achter-trumps-handelsbeleid/.

[7] ‘All Employees, Manufacturing’, 6 March 2026, https://fred.stlouisfed.org/series/MANEMP.

[8] Federal Reserve Bank of St. Louis, ‘All Employees, Manufacturing’, 6 March 2026, https://fred.stlouisfed.org/series/MANEMP.

[9] UNIDO, The Future of Industrialization (2024), https://www.unido.org/sites/default/files/unido-publications/2024-11/The%20Future%20of%20Industrialization%20-%20Building%20Future-ready%20Industries%20to%20Turn%20Challenges%20into%20Sustainable%20Solutions.pdf.

[10] Eurostat, ‘Sold Production, Exports and Imports’; Global Times, ‘Sustained Economic Recovery Underpins Stable Employment in China’, 25 April 2024, https://www.globaltimes.cn/page/202404/1311279.shtml.

[11] The White House, ‘Adjusting Imports of Processed Critical Minerals and Their Derivative Products into the United States’, The White House, 14 January 2026, https://www.whitehouse.gov/presidential-actions/2026/01/adjusting-imports-of-processed-critical-minerals-and-their-derivative-products-into-the-united-states/; The White House, ‘ADJUSTING IMPORTS OF SEMICONDUCTORS, SEMICONDUCTOR MANUFACTURING EQUIPMENT, AND THEIR DERIVATIVE PRODUCTS INTO THE UNITED STATES’, The White House, 14 January 2026, https://www.whitehouse.gov/presidential-actions/2026/01/adjusting-imports-of-semiconductors-semiconductor-manufacturing-equipment-and-their-derivative-products-into-the-united-states/; Congress.gov, ‘U.S. Commercial Shipbuilding in a Global Context’, legislation, 15 November 2023, https://www.congress.gov/crs-product/IF12534.

[12] The White House, ‘Regulating Imports with a Reciprocal Tariff to Rectify Trade Practices That Contribute to Large and Persistent Annual United States Goods Trade Deficits’, 2 April 2025, https://www.whitehouse.gov/presidential-actions/2025/04/regulating-imports-with-a-reciprocal-tariff-to-rectify-trade-practices-that-contribute-to-large-and-persistent-annual-united-states-goods-trade-deficits/.

[13] Council on Foreign Relations, ‘A Guide to Trump’s Section 232 Tariffs, in Maps’, 14 November 2025, https://www.cfr.org/articles/guide-trumps-section-232-tariffs-nine-maps.

[14] Council on Foreign Relations, ‘Tracking Trump’s Trade Deals’, 17 March 2026, https://www.cfr.org/articles/tracking-trumps-trade-deals.

[15] Politico, ‘Thousands of Carve-Outs, Caveats Weaken Trump’s Emergency Tariffs’, 15 December 2025, https://subscriber.politicopro.com/article/eenews/2025/12/15/trump-tariff-exemptions-us-imports-data-ee-00685168.

[16] Amiti et al., ‘Who Is Paying for the 2025 U.S. Tariffs?’

[17] Global Trade Alert, ‘Section 122 in Effect: What the US Tariff Regime Looks like Now’, 21 February 2026, https://globaltradealert.org/reports/S122-US-Tariff-Estimates.

[18] Federal Reserve Bank of St. Louis, ‘Total Construction Spending: Manufacturing in the United States’, 23 March 2026, https://fred.stlouisfed.org/series/TLMFGCONS; Federal Reserve Bank of St. Louis, ‘Private Fixed Investment: Nonresidential: Structures: Manufacturing’, 13 March 2026, https://fred.stlouisfed.org/series/C307RC1Q027SBEA.

[19] Federal Reserve Bank of St. Louis, ‘All Employees, Manufacturing’.

[20] Federal Reserve Bank of St. Louis, ‘Feb 2026, Industrial Production Indexes: Market and Industry Group: Monthly, Seasonally Adjusted’, accessed 30 March 2026, https://fred.stlouisfed.org/release/tables?eid=49745&rid=13.

[21] Federal Reserve Bank of St. Louis, ‘Feb 2026, Industrial Production Indexes: Market and Industry Group: Monthly, Seasonally Adjusted’.

[22] Lin Jones et al., Determinants of Intermediate Trade, 18 December 2025, https://www.researchgate.net/publication/399769978_Determinants_of_Intermediate_Trade.

[23] WITS, ‘Trade Statistics by Country’, 2023, https://wits.worldbank.org/countrystats.aspx?lang=en.

[24] Federal Reserve Bank of St. Louis, ‘Job Openings: Manufacturing’, 13 March 2026, https://fred.stlouisfed.org/series/JTS3000JOL; Federal Reserve Bank of St. Louis, ‘All Employees, Manufacturing’.

[25] Deloitte Insights, ‘Taking Charge: Manufacturers Support Growth with Active Workforce Strategies’, 3 April 2024, https://www.deloitte.com/us/en/insights/industry/manufacturing-industrial-products/supporting-us-manufacturing-growth-amid-workforce-challenges.html.

[26] Census.gov, ‘Foreign-Born: 2024 Current Population Survey Detailed Tables’, Census.Gov, accessed 30 March 2026, https://www.census.gov/data/tables/2024/demo/foreign-born/cps-2024.html.

[27] ‘The Chipmakers’, Center for Security and Emerging Technology, September 2020, https://cset.georgetown.edu/publication/the-chipmakers-u-s-strengths-and-priorities-for-the-high-end-semiconductor-workforce/; Semiconductor Industry Association, Chipping Away: Assessing and Addressing the Labor Market Gap Facing the U.S. Semiconductor Industry, July 2023, http://www.semiconductors.org/chipping-away-assessing-and-addressing-the-labor-market-gap-facing-the-u-s-semiconductor-industry/; John Liu, ‘What Works in Taiwan Doesn’t Always in Arizona, a Chipmaking Giant Learns’, Business, The New York Times, 8 August 2024, https://www.nytimes.com/2024/08/08/business/tsmc-phoenix-arizona-semiconductor.html.

[28] National Defense Industrial Association, ‘National Security Experts Call on Congress to Keep STEM Talent in the US’, 10 May 2022, https://www.ndia.org/about/press/press-releases/2022/5/10/letter.

[29] Dario Caldara et al., ‘The Economic Effects of Trade Policy Uncertainty’, International Finance Discussion Papers, International Finance Discussion Papers, September 2019, 1256, https://ideas.repec.org//p/fip/fedgif/1256.html.

[30] Economic Policy Uncertainty, ‘US EPU (Monthly, Daily, Categorical)’, accessed 30 March 2026, https://www.policyuncertainty.com/us_monthly.html.

[31] Cato Institute, ‘Tariff “Inclusion” Process Comes with High Costs, Absurd Outcomes, and Extra Cronyism’, 22 August 2025, https://www.cato.org/blog/tariff-inclusion-process-comes-high-costs-absurd-outcomes-extra-cronyism.

Experts

Related Content