")

As EU leaders gather in Brussels to discuss trade policy, Germany finds itself caught between dependence on China and the growing costs of economic engagement. While German industries remain deeply tied to the Chinese market, China’s push for domestic alternatives and growing competitiveness in high-tech manufacturing are eroding the benefits of this relationship. With Germany’s key industrial sectors now running trade deficits and political pressures mounting at home, Berlin’s choices will shape not only its own future but also the direction of EU trade policy, writes Ron Stoop, Strategic Analyst Geo-economics, in a new HCSS Expert Analysis.

This Thursday, the EU heads of state meet in Brussels for two days to discuss a slate of hot-button topics. One of the topics being discussed is the EU’s trade policy towards other countries, particularly China.

Europe’s relationship with China has soured in recent years. Reciprocal salvos of warnings and restrictions have raised the stakes for both the EU and China. For the EU, much is at risk: China has emerged as a dominant force in global manufacturing, pushing European legacy companies onto the defensive. The EU depends on China for critical inputs while China increasingly outcompetes it in the high-tech goods that European growth is built on, such as cars, telecoms equipment, and electronics. For export-reliant member states, the threat is existential.

No country feels the pressure as directly as Germany. It has long been globally dominant in automotive, chemicals and machinery, the country’s ‘heartland sectors’. These industries employ millions of Germans and sustain an EU-wide network of suppliers and small businesses.

Given these trends, one would expect Germany to be squarely in favour of more protective measures to defend its industrial interests. Counterintuitively, Germany’s position has been hesitant. Chancellor Merz has oscillated between courting Xi Jinping in person, alongside a host of business representatives, and condemning the EU-China trade relationship as ‘not healthy‘.

In short, Germany is torn between competing interests. On the one hand, its industries are suffering from Chinese competition, denting not only domestic production but also a sense of national economic pride. On the other hand, German companies are deeply embedded in China, with the country serving not only as a production base but also as an important target market.

However, many trends suggest the upsides of engagement with China are disappearing, while the downsides are becoming more harmful. For one, the idea of China as a massive demand market is disappearing. China is actively encouraging the choice for domestic alternatives in public and corporate procurement. In 2023, iPhones were banned for Chinese bureaucrats – with Huawei becoming the new brand of choice. Simultaneously, Westerns companies are experiencing several barriers to procurement contracts or market access. Slowly, the earning opportunities are disappearing.

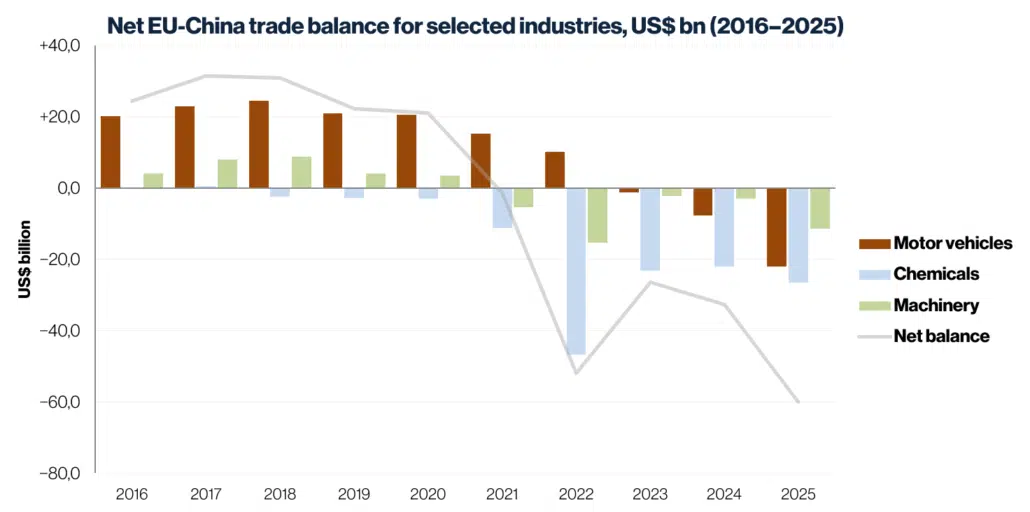

Meanwhile, the downsides are real. The structural decline in Germany’s trade position is best seen in the trajectory of its most important manufacturing industries. A decade ago, EU exports in motor vehicles and machinery were still significantly positive, with chemicals achieving a small net positive trade balance in 2016 and 2017 (see figure 1). That all changed in the wake of the Covid-19 crisis: this period shows a structural change in European export patterns. 2023 was the decisive break year: all three product groups products turned negative. Personal vehicles, heavy machinery, car parts, harvest machines, chemical precursor materials and batteries started entering the EU internal market en masse. This trend persisted in 2024 and 2025, pushing the balance of these ‘heartland’ goods towards a net deficit of roughly 60 billion dollars in 2025. In terms of employment, Germany dominates these sectors within Europe, and is therefore likely to experience much of its economic fallout.

Figure 1: Germany’s heartland sectors all turn negative in 2023 | Data: ITC Trade Map

Absent a structural rebalancing of the EU-China trade relationship, Germany will suffer economically and politically. Economically, since Germany’s growth model is already sputtering, with its GDP barely growing since 2022. Politically, since the AfD is gaining traction among disaffected voters, and studies show that economic malaise generally benefits the far right. This could create political instability in Germany that would reverberate through the whole of Europe, since many EU member states already struggle with political radicalism themselves.

Without Germany’s leading voice, a strong EU policy can hardly be expected. Hopefully, upcoming Thursday the economic ‘Zeitenwende’ will finally take place, with Germany at the helm, or at least not hitting the brakes.

Ron Stoop, Strategic Analyst Geo-economics

Experts

Related Content